Applied Financial Planning Certification Exam 1 (AFP) Questions and Answers

Derek recently inherited $900,000. He asks his financial planner to invest the entire amount in a concentrated portfolio of junior mining stocks. Derek has never invested before, has two young children, and is still deciding whether to purchase a home. What should the planner do first?

Evan meets with his financial planner to review his concerns around inflation and its impact on his TFSA investment portfolio. His financial planner researches the current holdings and recommends that he sells one of the portfolio’s equity funds. Which replacement option should the financial planner recommend to Evan?

A business owner completes an estate freeze, taking back preferred shares with a fixed redemption value while children receive common shares. What is a primary risk of this strategy for the owner?

How should Jenny, a financial planner, explain the benefits of a fee for service method of compensation to a prospective client?

A client completed a financial plan two years ago. Since then, she has divorced, changed jobs, and purchased a new home. What is the planner’s most appropriate recommendation?

Ali wishes to retire in five years. His financial planner calculates that he needs to save an additional $40,000 to meet his retirement income objectives. What would Ali’s financial planner advise him to do in order to meet his retirement income objectives?

Jelena, age 32, is single and works as a partner in a law firm. She is meeting with her financial planner, May, as she would like to start investing. Her friend John talks about hot sectors in the stock markets and has recently brought up the cannabis sector. She has done some reading about this sector and is willing to experience large decline in her investments. Jelena also mentioned to May that she believes in high long-term returns. What conclusion can May draw based on their discussions about the stock market and Jelena's expectations?

Jonah is meeting with his client, Muhsina, who owns Myke Inc., a Canadian-controlled private corporation. Based on current market value, if he decides to sell Myke Inc., Muhsina will have a capital gain of $400.000. He expects the value of Myke Inc. to increase in future years and has a CNIL balance of $100,000. He wants the future increase in value to be taxed in the hands of his children, Teshi and Kaliyah, and to minimize the cost. What action should Jonah advise Muhsina to take to meet his goal?

Which statement best distinguishes a defined benefit pension plan from a defined contribution pension plan?

What information is least important for Harry as a financial planner in his assessment for insurance coverage for his client with respect to estate planning purposes?

Rosa has just learned that her daughter Marissa, age 23, does not intend to return to university. She has been saving for her daughter's education since Marissa was 10 and is concerned there will be a significant tax liability. How should Rosa's financial planner advise her to utilize the funds when she redeems the RESP in order to offset the tax liability?

Keitaro wants his spouse to receive income from his assets for life after his death, but wants the remaining capital to pass to his children from a prior marriage after the spouse dies. Which strategy best fits this objective?

Owen and Lina are looking to purchase a home in the next few months. Owen is the primary income earner for the family. His credit history is weak with several recently paid collections Lina has a perfect credit record but limited income and irregular employment. What will their financial planner advise them about the impact their credit ratings will have on their ability to secure a mortgage?

Alexander and Irena, age 30 and 32 respectively, are married and have been working full-time for one year. They have a daughter, age 3, and are expecting their second child. They recently bought a home with a mortgage balance of $390,000 at 4% amortized over 25 years. Their financial planner is trying to determine their tolerance for risk. After completing the life-cycle analysis, how can their financial planner explain the stage in which the couple finds themselves and the risk tolerance associated with it?

Priya grants her brother trading authority over her non-registered investment account. Her brother calls the financial planner and asks for Priya’s full net worth statement, tax return, and beneficiary information so he can “help with planning.” What should the planner do?

Mark, a financial planner, is meeting his client Adam for the first time. From the conversation, Mark learned that Adam has some experience on trading stocks. Adam asked Mark to explain about efficient market theory that he overheard a colleague talking about a few days ago. How should Mark respond to Adam's question in simple terms?

A client’s portfolio target is 50% equities and 50% fixed income. After a strong equity market, the portfolio is now 68% equities. The client’s circumstances and objectives have not changed. What should the planner recommend?

Francois and Brigitte are meeting with their financial planner, Robin. They would like to ensure that if one of them were to die suddenly that their mortgage would be paid in full. Their current mortgage has an outstanding balance of $400,000 with 10 years remaining. The couple are in good health and have a well-balanced financial plan that focuses on debt reduction and savings. Which type of insurance policy should Robin recommend to assist the couple in meeting their objective?

Sheeba is a financial planner and meeting with Ivana, a new client. She explains that part of her process is to recommend products and services, but prior to doing so, she will closely investigate the options to ensure they match up with Ivana's goals. Which professional responsibility has Sheeba demonstrated to Ivana?

Miles tells Rasheed, his financial planner, that he would like to assign the growth assets in his portfolio to his children. Rasheed recommends Miles freeze his estate. What is the primary risk associated with an estate freeze?

Maya, a financial planner, is meeting with a new client who was recently referred to her. In determining the client's overall risk tolerance, what qualitative data should Maya capture as part of her process?

A married couple has a $480,000 mortgage with 15 years remaining. They want the mortgage retired if either spouse dies during that period. What insurance structure best fits this objective?

Ronny, a successful business owner, established a discretionary family trust earlier this year as a means to split income with his children. Ronny's children are both under the age of five and are both income and capital beneficiaries of the trust. He is concerned that the 21-year rule will result in a significant amount of tax resulting from unrealized capital gains. What strategy would be best if Ronny's goal is to minimize the total amount of tax payable by the trust and/or beneficiaries at the 21-year mark?

Bill was recently declined for a loan application at his financial institution, and he is concerned that a liability has been added to his credit bureau that does not belong to him. He asks his financial planner to review his credit bureau with him to help him identify why he may have been declined. Which area of the credit bureau might his financial planner advise Bill to review?

A client realizes a $16,000 capital loss on one non-registered investment and a $28,000 capital gain on another non-registered investment in the same year. How should the loss be treated?

In 2019, Glenda, age 46, visited her financial planner to discuss her goal of retiring at the age of 65. Glenda had questions about whether she qualified for the maximum amount of CPP and OAS benefits as she had immigrated to Canada just 10 years earlier to take a job as a nuclear technician. What should her financial planner have told her?

A higher-income spouse contributes to a spousal RRSP for the lower-income spouse. The lower-income spouse withdraws the contribution amount the following year. What should the planner warn them about?

A client sends an email alleging that a mutual fund recommendation was unsuitable because the fund declined sharply after purchase. The client asks for compensation. What is the financial planner’s first professional obligation?

Mary, an accredited financial planner, recently met with clients Michael and Radha. They are high- net-worth clients who are in their mid-40s. Michael is a heavy equipment operator at a local oil field, and Radha is a homemaker. They are ready to retire in 10 years and very excited to start planning for the next chapter in their lives. Mary explained her planning process, her accreditation, and her remuneration. When Mary presented the client agreement letter, both clients were surprised. They said they did not know why they would sign a letter to get advice on their own finances. How should Mary answer their question?

A retiree receives income-tested benefits and needs occasional withdrawals for vacations and home repairs. Which account is generally most efficient for withdrawals that do not increase taxable income?

A financial planner, Rachel, is preparing to recommend a discretionary portfolio manager to her client. The portfolio manager is owned by Rachel’s former employer, and Rachel receives no referral fee. However, the former employer regularly sends new clients to Rachel’s practice. What should Rachel do before making the recommendation?

A client refuses to provide details about debt balances, tax returns, and monthly expenses but asks the planner to confirm whether retirement at age 55 is achievable. What should the planner do?

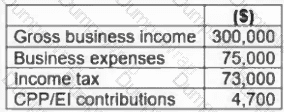

Jackson, a wealth advisor, is helping Terry, a self-employed IT professional, determine his net income. The goal is to develop a budget and savings strategy for the year ahead Terry has provided the information below:

What is Terry’s net business income?

A client says, “I want to retire comfortably as soon as possible.” Which response best reflects the financial planning process?

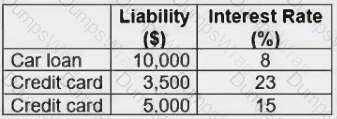

Justis, age 62, and his wife Jen, age 58, are meeting with their financial planner, Luke. They are both planning to retire by age 65. Their goals are to minimize debt and reduce taxes. The couple's financial situation is outlined below.

Justis' annual income is $25,000. He has a $15,000 RRSP, $30,000 single non-registered account and a $25,000 TFSA. Jen's annual income is $60,000, and she has a $150,000 RRSP, $50,000 single non-registered account and a $20,000 TFSA.

Jen's marginal tax rate is 35%, and Justis' is 25%. Assuming all investments are making interest income of 10%, what would be the most appropriate strategy for Luke to recommend for the couple?