Life License Qualification Program (LLQP) Questions and Answers

Andrea, owner of Andrea’s Fashions Inc., employs her designer daughter Judy, who will carry on the business after Andrea is gone. Wishing to ensure that the business would not suffer financially when Andrea passes away, Andrea decides at age 50 to have her business own, pay for, and be the beneficiary of life insurance on Andrea's life. The type of insurance that best suits is non-convertible Term 10 life insurance renewable until age 80.

What should her life insurance agent advise regarding this policy?

Anita is a 50-year-old woman who is thinking of purchasing a $150,000 permanent life insurance policy to pay for the capital gains tax that will be payable on her country home upon her death. She had purchased the home twelve years ago and wants to bequeath the property to her niece when she dies.

Which of the following features about a permanent insurance policy is TRUE?

Coraline owns a $250,000 whole life insurance policy. She purchased the policy last year and does not have any funds accumulated in her cash surrender value (CSV). On December 30, Coraline assigns the policy to the cancer foundation, and she plans on continuing to pay the $200 monthly premium. Coraline calls her accountant James to ask him how much of her donation she will be able to use to obtain a charitable tax credit this year.

Donald finds out from his doctor that he only has about 10 months to live. He owns a $100,000 life insurance policy with a terminal illness benefit of $50,000. Donald has named Yvana as the policy's irrevocable beneficiary.

Donald wants to know whether he has to obtain Yvana's consent concerning the amount he will be paid as the terminal illness benefit. He would also like to know how much Yvana will receive after his death.

What should his insurance agent tell him?

Three years ago, Douglas purchased a whole life insurance policy with numerous supplementary benefits and riders. Today, he meets with his doctor who informs him that he has late-stage colon cancer and has only a few months to live. Even with surgery, his chances of survival are low. Douglas calls his insurance agent, Penny, to ask her what he should do to obtain a benefit immediately.

Six years ago, when Kacey was working as an active firefighter, she purchased a $200,000 30-year term life insurance policy. At the time, the insurance company rated her policy. Recently, she changed roles and now works for the fire department’s public relations office, answering media calls and filling out paperwork. She meets with her insurance agent, Bernice, to ask if the insurer would consider reducing her premiums.

Ben and Pam, both aged 37, are married with three young triplets, Lucas, Jack, and William. Ben works as a pharmaceutical rep, and Pam is a stay-at-home mom. Ben’s monthly salary is $6,000. An unforeseen accident happening, where Ben were to die, would leave Pam and the kids in serious financial trouble. Ben and Pam want to address this, so they meet with a licensed life insurance agent to discuss purchasing a life insurance policy. The agent, assuming an interest rate of 4%, shows Ben and Pam the capitalized value of his lost income.

Based on the above information, using the income replacement approach, how much life insurance does Ben need?

Bea is a married 65-year-old woman applying for a life insurance policy. She meets with Stanley, her insurance agent, to review her insurance needs. Stanley inquires if Bea has started receiving Old Age Security (OAS) and Canada Pension Plan (CPP) benefits. Why is it important for Stanley to know this?

Sidney is a professional hockey player that recently purchased a large house and wants to have life insurance coverage to cover the cost. He meets with his life insurance agent, Dave, to determine his need and complete an application. After completing a needs analysis, it is determined he should have $25,000,000 worth of life insurance. Dave makes an application to A-Z Life Insurance Co. for $25,000,000 of permanent life insurance. The insurance company tells Dave that they have a maximum retention amount of $20,000,000 per policy.

What will happen in Sidney's case?

Svetlana is a 45-year-old single mother with two children: Georgi 17; and Ingrid 13. The children's father, Vladimir, has a serious gambling problem and only visits them sporadically. Vladimir's younger brother Sergei, on the other hand, is a dependable and helpful uncle who helps Svetlana regularly with the children. Svetlana meets with Robert, an insurance agent to review her life insurance needs because she wants to make sure that her children are taken care of if she were to die prematurely. Robert suggests that she purchase a $200,000 policy. Who should she name as a beneficiary?

Elizabeth has a universal life policy and has been diligent in funding it over the last several years. As a part of this, the investment account within the policy has done quite well. Elizabeth met with her financial advisor as she would like a refresher on the benefits of the accumulating fund, as it has been a while since they last discussed this; flexibility with and access to cash flow are important to her as she would like to use this as part of her retirement planning in the future.

What benefits of the accumulating account apply to Elizabeth's situation?

Antonin and Magali are common-law partners in their thirties. They have two children together: a five-year-old daughter and a two-year-old son. Divorced from ex-wife Vanina, Antonin must pay her $1,500 a month in child support until their 10-year-old son reaches 25 years of age. Antonin is covered under a group life insurance policy equal to one year of his $75,000 annual salary. Magali does not currently earn any income, as she takes care of their two children full-time. Antonin is the sole owner of their residence, which will be fully paid off in 25 years.

What life insurance coverage do Antonin and Magali need in their situation?

Oliver, an insurance agent, meets with Roman and Julie. They are a married couple with a five-year-old son William. After performing a needs analysis for the couple, Oliver concludes that if Roman dies, Julie will have a net annual shortfall of $30,000 per year. Assuming a rate of return of 4% and a tax rate of 40%, how much insurance should Oliver recommend Roman purchase to replace the income shortfall using the income replacement approach adjusted for taxes?

A black and white math equation Description automatically generated with medium confidence

A black and white math equation Description automatically generated with medium confidence A number with numbers and lines Description automatically generated with medium confidence

A number with numbers and lines Description automatically generated with medium confidenceGary owns a $500,000 T-20 life insurance policy with an accidental death rider of $250,000. His estate is named as beneficiary. Gary dies when his car falls into a lake. The autopsy shows that he had a heart attack, which caused his death and led to the accident.

What death benefit amount will the life insurance company pay Gary's estate?

Pete is the owner of Blenheim News Tribune Inc, a company responsible for producing the local newspaper. He has owned the family-run business for 30 years, and he currently employs 10 people. Peter wants to offer a group benefits plan to his staff, so he meets with Daphne, a licensed insurance agent to go over some options. He would be willing to cover 75% of each employee’s required premium and ask that each employee be responsible for their remaining 25%.

Based on the information provided, which statement is true regarding Blenheim News Tribune Inc's group insurance premiums?

Rhonda is a sixty-year-old biologist at the local university. She has two adult children Connor and Daniel. She meets her life insurance agent Todd to make sure that if something were to happen to her that everything would be taken care of. She has taken the initiative to have a will done that has all of her assets divided between her two children after any debts or taxes are settled. She knows her boys are not great with money so she names her friend Sandra as the executor.

One of the things that Rhonda is concerned about is the taxes that will be owed on her final tax return and thinks a life insurance policy would be a good idea to solve her issue.

What should Todd recommend while completing a life insurance policy to make sure that Rhonda’s concerns are met?

Akeno is a 65-year-old retired accountant. He is divorced and has a 40-year-old son who is financially independent. Thanks to years of diligent savings, Akeno now enjoys a comfortable retirement. In addition to his pension income, he has over $300,000 invested in shares in his non-registered account. He lives in a mortgage-free home valued at $700,000 and owns a cottage valued at $500,000. The mortgage on the cottage is $100,000. Akeno purchased the homes 30 years ago when housing prices were low. It is important to him to donate $100,000 to the Alzheimer's Association when he dies. What is the GREATEST financial risk that would arise in the event of Akeno’s death?

Axel owns a $150,000 whole life insurance policy with an accumulated cash surrender value (CSV) of $20,000. His monthly premiums are $300, due on the fifth day of each month. Axel misses his November 5 premium payment and then dies a few weeks later, on November 20.

Life insurance agent Alexandra completes a life insurance application with her client, Joshua. After three months in underwriting, the application is accepted and the policy is issued on a standard rate. Alexandra goes to deliver the policy. When she gets to Joshua's, he tells her how he just got out of the hospital with a serious blood clot.

What should Alexandra do?

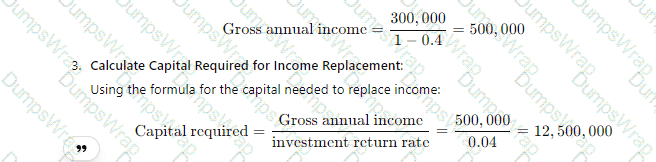

Jasper is the sole breadwinner in his family. His wife Stephanie has chosen to dedicate all of her time to raising their 3 young children. Luckily, Jasper earns a monthly after-tax income of $25,000 working as a family doctor in the local clinic. Jasper meets with his insurance agent Odda to purchase a life insurance policy that will ensure his family will be able to continue to enjoy their current lifestyle in the event of his death. If his average tax rate is 40% and the investment return is 4%, how much life insurance should Jasper purchase based on the income replacement approach?

A close-up of a math Description automatically generated

A close-up of a math Description automatically generatedLarson, an insurance agent, meets with Julia, a real estate agent, to review her insurance needs. Julia has $500 in her savings account and does not own a tax-free savings account (TFSA) or registered retirement savings plan (RRSP). She earns an average of $150,000 a year in sales commissions and rental income from two condo units she owns. The combined value of her income properties is $1,000,000, and the mortgage is $200,000.

Larson recommends that Julia open a TFSA and use it to invest $400 a month in a money market fund.

Which of the following personal risks is Larson trying to mitigate with this advice?

Mathilde, aged 65, is seriously ill—though still mentally competent. She has therefore granted her son Jim power of attorney for property so that he will help manage her investments. She has contacted her life insurance agent, asking him to gather all the information needed to:

Transfer money from her balanced segregated fund into an income fund, and

Convert her RRIF into a life annuity.Some signatures are required to complete the transactions.

With his power of attorney, what can Jim do if he goes to the agent’s office by himself?

Mohammed is an employee at Optima Plus Inc. Over the years, he accumulated $15,000 in the company's group plan. He knows that his contributions into the plan are not tax-deductible, and he is not taxed on the funds when he makes a withdrawal.

What type of plan does Mohammed have with his employer?

(Arthur's assets include a home worth $744,000, savings of $41,000, and a whole life insurance policy with a death benefit of $300,000 and a cash value of $196,000. His liabilities include a $150,000 reverse mortgage and $2,090 income tax owed.

What is Arthur's net worth?)

Leonard and Ashley, a couple in their early 30s, meet with Howard, an insurance agent, to review their investment needs. Leonard earns $60,000 a year as a research physicist, and Ashley earns $25,000 as an actress. They each have $3,000 in their respective chequing accounts. Leonard also has $40,000 invested in his group registered retirement savings plan (RRSP). Ashley has a Subaru WRX worth $20,000 with a car loan of $10,000. Leonard does not own a car, but he has an outstanding student loan of $30,000.

What is the couple's net worth?

(Philip is applying for a segregated fund contract and must choose a sales charge. He does not foresee needing withdrawals and wants minimal management expenses and no initial reductions or penalties.

Which form of sales charge would best suit Philip?)

Janice meets with Patrick, an insurance agent, to review her investment needs. Patrick suggests that she invest in segregated funds. Janice is not familiar with these types of funds.

What information can Patrick provide to Janice to help her understand the advantages of segregated funds?

Hana, a 25-year-old personal assistant, recently got a job where the employer offers all employees access to a defined contribution pension plan (DCPP). Hana meets with the group insurance agent, Tom, because she must choose her investments and she doesn't know what she should choose. She is not very knowledgeable about investments, but since the money will only be used at retirement, she wants to invest in a fund that combines stocks and bonds and that is easy to understand.

Which fund should Tom suggest?

Geneviève has won $100,000 in the lottery and now wants to invest this amount. She has a very good risk tolerance and a long-term investment horizon. Furthermore, Geneviève—who works for a firm of economists—is convinced that interest rates will rise on a regular basis over the next 10 years and is firm in her requirement that these interest rate increases not affect her investments, insofar as possible.

What kind of investment, from among the following, could be suitable for Geneviève?

Lydia, a 73-year-old retiree, has a large lump sum of non-registered money she intends to leave to her grandchildren upon her death. She has no need of this money personally, because she already benefits from a generous work pension and owns a sizeable RRIF. She wants to invest that lump sum in such a way that the capital is protected. She hopes it can grow in the long run when the market does well. As the investment grows, Lydia would like to have the opportunity to lock in the gains.

Which of the following investments would be most appropriate for her?

(Philippe, age 50, has been a widower for six months. He inherited the money in his wife's pension fund, which he transferred to a LIRA. He also received a $150,000 life insurance benefit. Philippe works for a private firm as an IT analyst and earns $80,000 a year. He would like to retire at age 60.

What income sources will be available to Philippe if he retires at age 60?)

George, aged 72, has a number of medical conditions related to smoking and diabetes. He is planning the distribution of his estate, which is valued at $1.1 million. He will invest $1 million in a segregated fund and name his two daughters as equal beneficiaries. The remainder of the estate will go to George’s favourite charity. George has peace of mind knowing that even if markets are down at the time of his death, his daughters will together receive an inheritance greater than the charity.

What unique feature of segregated funds has enabled George to formulate his estate plan in this way?

Julie is a stay-at-home single parent with an eight-year-old son, Justin, who has severe intellectual disabilities. Julie’s mother, Lucille, who died recently, used to help Julie financially, especially for Justin’s special needs. She wanted this assistance to continue after her death. To this end, she designated Justin as beneficiary of her RRSP, now worth about $100,000. Julie would like this amount to be transferred to a plan that would eventually provide Justin with an annual income, which she would administer. She would like a plan that is eligible for government grants.

To which plan should Julie transfer the funds?

(Beth, aged 73, has a RRIF with a current market value of $380,000. The account is managed by her bank, and Beth has been disappointed with its performance so far. She is therefore thinking of transferring the RRIF to her insurance company and purchasing a registered annuity with those funds.

This would be the first time Beth is making an investment outside of the bank environment. She wonders what kind of information the insurance agent would keep on file to document the transaction.

To process the application and comply with FINTRAC requirements, which of the following records would the agent need to create and keep on file?)

Janice, age 73, plans on purchasing a joint-and-last-to-die annuity. She wants to receive the highest possible annuity payments.

Who should be the joint annuitant?

(Joe and Joy, both aged 65, have $280,000 in savings and a $200,000 joint first-to-die life insurance policy. They want to buy an annuity to provide steady income in retirement.

What type of annuity would best suit their needs?)

Planet Source decides to implement a defined contribution pension plan (DCPP) for its 75 employees. The company's president appoints Josie, the human resources director, as the plan administrator.

Which of the following BEST describes Josie's responsibility as a plan administrator?

Germaine, a shareholder-manager of a large firm, set up a group RRSP for her business several years ago. As the company has been very successful, she now wants to set up a second group savings plan for her employees. She would like this new plan to allow employees to withdraw money at any time without incurring additional income tax or other penalties.

Which one of the following plans would best fit Germaine’s requirements?

Davy, who just turned 55, intends to retire 10 years from now. Together with his life insurance agent, he determines that he will need to have approximately $200,000 in RRSPs when he reaches age 65 in order to retire comfortably. He feels confident that his current RRSP account can generate a return of 3% per year on average for the next 10 years. However, he does not plan to contribute any new funds to his RRSP because he wants to start saving in his TFSA account instead. He therefore wonders whether his RRSP account currently has sufficient funds for him to meet his retirement goal in 10 years.

What is the minimum RRSP account balance needed now for Davy to meet his goal? (Round to the nearest dollar.)

(Ten years ago, Yamina invested $2,500 in a segregated fund contract with a 75%/100% guarantee structure. The market value of the contract peaked at $4,500 but then fell. Now, at maturity, the units are worth $2,250.

How much can Yamina expect to receive?)

Arianna has been an insurance agent with Ideal Life for over 15 years, always working hard to grow her client base and keep her existing clients happy. Last week, she prepared an elaborate insurance plan for Raphael, a potential new client. But when they meet, Raphael tells her he wants a second opinion. Arianna tells him that she cannot allow him to show or discuss details of her work with a potential competitor. She explains it's wrong for another agent to benefit from her work and knowledge.

Which of the following standards of conduct did Arianna contravene?

Cassie applies for a $100,000 renewable 10-year term insurance policy through Mason, her insurance of persons representative. A month later, when Mason meets with Cassie again to deliver her contract, Cassie says she had to have a biopsy the previous week for a persistent cough. Mason tells her not to worry because the policy is already accepted. He completes the policy delivery. Six months later, Mason receives a call from Cassie's boyfriend informing him that Cassie died of stage 4 throat cancer.

How will the insurance company handle the claim?

After completing a thorough needs analysis, Dimitri, an insurance agent with Health Assure, recommends that his client Chandler purchase a deferred annuity contract and contribute monthly to a balanced segregated fund to build up savings that Chandler can use as retirement income. Dimitri explains to Chandler that the type of annuity contract he is recommending has two distinct phases.

What are those two phases?

Ontario residents, Juan and Maria, are a married couple approaching retirement. They have askedtheir representative Carlow to review the details of Maria’s defined benefit plan (DBPP).

Which of the following statements about Maria’s pension is CORRECT?

After working nine years as an insurance agent, Jamie decides to make a change in her life and go back to school. A colleague she used to work with on personal health insurance congratulates her and tells her that he will pay her a flat fee for every health insurance referral she makes to him, as long as the referral results in a sale. What could be said about this referral arrangement?

Dale meets with his last appointment of a busy workday. He is helping his client Larry fill out a disability insurance claim form. Larry suffered a heart attack a week ago and is at home recuperating. Larry will be unable to work for the next 6 months and needs the benefits as soon as possible to cover his expenses. The at-home appointment takes a little longer than scheduled and Dale finds himself rushing to his son’s big hockey tournament. In his haste, he puts Larry’s form in his briefcase and subsequently forgets to submit the form. Which responsibility did Dale breach?

Everett is an insurance of persons representative who works exclusively for Moon Life Insurance. He wants to leave the company and become an independent representative. He knows that before he branches out on his own, he needs to ensure he has sufficient liability insurance.

Which of the following statements about his professional liability insurance is CORRECT?

Danny purchases a $1,000,000 whole life insurance policy. He names his three daughters, Donna-Joe, Stephanie, and Michelle, as revocable beneficiaries with each receiving one-third of the death benefit.

If Michelle predeceases Danny, and Danny did not have a chance to modify his beneficiary designation, how will Danny’s death benefit be paid out?

Mark and Jesse had a joint life insurance policy which they purchased on the advice of their insurance agent, recognizing that if one of them died, the other would need an insurance benefit to pay off their mortgage and for final expenses. Coverage is $450,000. Last week their car went off the road in a snowstorm. Both were declared dead at the scene. The two had named their adult nephew, Louis, as contingent beneficiary. What is the amount of the benefit the insurer will pay Louis?

After meeting with his advisor Monica, Tom agrees to apply for a $50,000 whole life insurance policy. Monica tells him that the monthly premium will be $40 per month. Monica is advised by underwriting that Tom qualifies for an additional $10,000 critical illness rider, and that the new premium would be $50 per month. Monica advises underwriting that Tom accepts the additional coverage without speaking with him first, because it is such a good deal and great coverage, he won’t mind. When Tom finds out what she has accepted on his behalf, without his knowledge, he is upset and wants to lodge a complaint to someone other than the insurance company and Monica; he wants to speak with an independent third party. He finds the contact information for the local regulatory authority. What are some of the responsibilities the regulatory authority has in protecting clients like Tom?

The primary and secondary beneficiaries of Rachel and Chad’s joint first-to-die permanent life insurance policy are each other and their adult children, respectively. Within a year of Rachel and Chad’s divorce, Rachel unexpectedly passes away. The policy beneficiaries remained as originally designated. Whose claim will be paid by the insurer?

When Tim and Patricia were common-law spouses, they met with an insurance agent, Aelia, to purchase life insurance policies of $100,000 each, naming each other as beneficiaries of their policies. Five years later, Patricia leaves Tim to be with her personal trainer, Thomas. A year later, Patricia and Thomas marry, and Patricia gives birth to their baby, Cedrick. Tragically, just before Cedrick's 12th birthday, Patricia dies in a fiery car crash. She never modified her beneficiary designation.

Shortly after the crash, Thomas calls Aelia to inform her that Patricia has died and that he wants to claim the death benefit on her life insurance policy.

Who will receive the $100,000 death benefit?

Last month, Suzanne purchased a life insurance policy from a local agent. The agent told her that the policy would accrue a cash value that she could draw from in her retirement years and that the premium would never increase. After recently meeting with a close friend, who is a retired insurance advisor, she was dismayed to learn that what was sold to her is in fact a term policy with no cash value. If Suzanne wishes to make a formal complaint against the agent, which authority can assist her in doing so?

Elizabeth is a seasoned insurance agent. She meets with Harold, a new agent, to help him better understand the industry and the processes that they must follow. Elizabeth tells Harold about a body that administers the regulatory system applicable to insurance intermediaries. Which of the following is Elizabeth referring to?

Barry, a life insurance agent, is meeting his client Diane who came to Canada 26 years ago. Diane is turning 60 years old and is considering purchasing a non-registered life annuity to supplement her retirement income. Barry presented the quote to her and it was quickly accepted. During the application process, he recorded Diane’s contact information, used her Social Insurance card to ascertain her identity, and collected a cheque of $120,000 from a joint account. The names written on the cheque were Diane and Geoffrey. Diane explained that this was a joint account with her brother. What should Barry do to comply with FINTRAC’s guidelines regarding ascertaining identity?

Emeka, a new insurance agent with Sunrise Insurance, meets with her client, Mosi. After analyzing Mosi's needs, Emeka determines that Mosi's current life insurance coverage with Starlight Insurance is more than sufficient. Nevertheless, she persuades Mosi to cancel his existing coverage and buy a new life insurance policy with Sunrise Insurance. She believes this is a good compromise because Mosi will have the coverage he needs, and the new transaction will pay her a commission. Which of the following offences did Emeka commit?

Nine months ago, Osvaldo was instructed by his insurance agent, Jane, to write a cheque to renew his life insurance. Jane put the cheque in her wallet. She lost her wallet the very same day and completely forgot about Osvaldo’s payment. Some time later, Osvaldo died in a tragic car accident. His family made a claim for the death benefit, but was denied because the policy had lapsed. Who will have to compensate Osvaldo’s family for the loss of death benefit?

Surjit and Rajbir get married in 2010 and Surjit names Rajbir as the irrevocable beneficiary of his life insurance contract. In 2017, the couple divorces amiably and Surjit meets with his insurance representative, Ivan, to review his plans. Surjit tells Ivan that he would like to keep Rajbir as his beneficiary. What should Ivan counsel his client to do?

Andre, an insurance agent, meets with his client Jasper to discuss his $150,000 whole life insurance policy. Jasper is deeply indebted and needs at least $40,000 to cover his debt. Andre tells him about a company he knows that will be willing to give him $75,000 if he assigns his policy to them. Did Andre act appropriately?

Last year, Ezekiel purchased a $100,000 life insurance policy and named his wife Jolene as an irrevocable beneficiary of the policy. Last week, Ezekiel returned home early from a business trip and decided to surprise his wife instead of calling ahead. He arrived at midnight and not wanting to wake her, entered the house from the back door and left the lights off. Not expecting the intruder to be her husband, Jolene stabbed him in the heart with a kitchen knife. She quickly realized her mistake and called 911. Unfortunately, Ezekiel died in the hospital from his wounds. The police deemed Ezekiel's death as accidental, and no charges were filed. Will the insurer pay the death benefit?

Gold, a financial security advisor, recently met with a wealthy client who needed tax advice. The client also wanted to draft a will and a mandate in case of incapacity. Eager to meet his client’s needs and make recommendations, he did not think it necessary to propose a meeting with the firm’s tax expert and notary. Towards whom has Gold breached his duties and obligations?

Danny purchases a $1,000,000 whole life insurance policy. He names his three daughters, Donna-Joe, Stephanie, and Michelle, as revocable beneficiaries with each receiving one-third of the death benefit.

If Michelle predeceases Danny, and Danny did not have a chance to modify his beneficiary designation, how will Danny’s death benefit be paid out?

Pierre is an insurance of persons representative. His new client, Carole, wishes to buy life insurance but wants to know everything about life insurance products before making a choice. What are Pierre’s responsibilities in this case?

Marietta receives a summons from the syndic of the CSF regarding an investigation into her associate. The summons was delivered to her office on May 2 and she took notice of it on May 4. The summons requires her to receive the syndic representative at her office on May 19 at 8:30 a.m. Marietta has already planned for and reserved a week off for a vacation abroad from May 15 to 22. She immediately emails the syndic representative to inform him that she will be out of the country and cannot be present on the 19th. She proposes meeting on the 14th or the 23rd of the same month. Pursuant to the Code of Ethics of the Chambre de la sécurité financière, which duties or obligations has Marietta breached?

Samya and Gary, who are both insurance representatives, are having lunch together. Gary has been very successful for several years and proposes a scheme to Samya to get insurance proposals signed for a fictional company they would create together. He believes that this system would make them millionaires in about ten years. Gary advises Samya to keep their conversation a secret. If Samya agrees to Gary’s proposal, what sanctions could she face?

Financial security advisor Juliette meets Pierre during a business meeting. Pierre gives her the name of a prospect, one of his friends. Juliette wants to start by contacting the prospect by email, then plans to follow up with a phone call to set up an appointment. Why should Juliette cease to proceed in this manner with her prospect?

Vasu, an insurance agent, meets with Francine, his new client. Francine wants to purchase a disability insurance policy. Vasu helps her complete the application form. In the process, he collects all the required medical and lifestyle information on his client and wonders what he must do with the information he collected.

Which of the following options is CORRECT?

Alexandre, a financial security advisor, recently left FinCode Inc. because of an unresolved dispute with the company. He is continuing his career as an independent advisor. This week, he has an appointment with a client who tells him that he met with another FinCode Inc. employee. However, that employee has a disciplinary record at the CSF for fraudulently copying a signature on a form. Since the client does not work in insurance and the information is public knowledge, Alexandre provides him with some clarification regarding the other advisor’s case. How can Alexandre encourage the client to do business with him without denigrating his competitor?

Alec is sure he sent his insurer his annual life insurance premium payment. The insurer did not receive it, however. The insurer then sent Alec a notice of non-payment of premiums, but Alec had moved in the meantime. Therefore, he never got the notice, even though he had emailed hisfinancial security advisor, Olivier, to inform him of his change of address. Unfortunately, Olivier was on a leave of absence and no one else in the firm took over the file. As a result, the policy lapsed. Alec sent Olivier’s firm several emails to complain, but no one responded. Which organization can Alec turn to?

Surjit and Rajbir got married in 2010, and Surjit named Rajbir as the irrevocable beneficiary of his life insurance contract. In 2017, the couple divorced amicably, and Surjit met with his insurance representative, Ivan, to review his plans. Surjit tells Ivan that he would like to keep Rajbir as his beneficiary.

What should Ivan counsel his client to do?

Patrick, an insurance of persons representative, gives a talk about his work to high school students. He tells them about his previous day’s activities. Which activity is considered ethical misconduct?

Insurance of persons advisor Somalia is careful to comply with the standards and regulations when she meets with potential clients. Under no circumstances would she want them to feel aggrieved or not respected. She makes sure to know their rights. Which legislation does Somalia not have to worry about?

Insurance of persons representative Véronique is meeting clients referred by an acquaintance for the first time. Observing some suspicious behaviours on their part, Véronique is thinking about reporting the transaction to the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). Which behaviours are signs of suspicious transactions?

Valerie, age 42, recently left her job after 15 years of service. She participated in a defined contribution pension plan and had accumulated benefits amounting to $88,000, eligible for transfer into a registered contract. What must Valerie do with this money?

Melissa, a La Tranquillité representative, is meeting with a client who tells her about something that happened to one of her friends. While she was taking part in an outdoor weekend at Mont-Tremblant Park, a forest fire broke out and one of the participants was never found. The client is about to take out life insurance with Melissa. She asks Melissa what would happen to her insurance capital in such a situation. What can Melissa tell the client?

President and sole shareholder of the Velos Tourisque company, Paul employs 50 people. Maryse, his financial security advisor, advises him to have his company take out life insurance on him. Who will be the parties to the contract?

A few months ago, Urmish filed a complaint to the Autorité des marchés financiers (AMF) about the services he received from his insurance agent, Jaba. The complaint was heard by the discipline committee, and Jaba was found guilty and ordered to pay a $10,000 fine. Jaba is upset and does not agree with the verdict. She would like to appeal the verdict.

Which of the following statements is CORRECT?

Benjamin is a financial security advisor working for the Larson Group. He is following a mandatory compliance training session given by Andrew, the compliance manager. Andrew explains the importance of following the Chambre de la sécurité financière code of ethics, and Benjamin would like to know to whom the code of ethics applies.

What is Andrew's CORRECT response?

Nathalie worked for 25 years as an administrative assistant at a manufacturing company. When she left the company 10 years ago, she transferred the money that she accumulated from the company’s pension plan into a locked-in retirement account (LIRA). Now she is 60 years of age and would like to withdraw the money from the LIRA.

Under which of the following circumstances would Nathalie be allowed to withdraw her funds?

Gino, an insurance of persons representative, is cleaning his office and going through old files. He comes across a file from a former client, Nathan, who owned a 20-year term insurance policy that was cancelled 3 years ago. Nathan now has a different representative and Gino no longer has any contact with him. Gino would like to know if he can destroy Nathan's file.

Which of the following options is CORRECT?

Wesley is a self-employed plumber. He meets with a licensed life insurance agent to explore his options regarding disability insurance. Wesley’s earnings have been stable over the past few years.His business generates gross income of $120,000 annually and write-off expenses of $30,000. Wesley’s average income tax rate is 30%. What income amount should be used to calculate the maximum disability benefits Wesley is entitled to?

Emery is a healthy wife and mother of two who spends her days caring for her children and volunteering at the local food bank. Emery would like to purchase disability insurance coverage because she is worried about how she would be able to take care of her family if she becomes disabled.

What type of disability policy, if any, is likely to be issued to her?

Alex, aged 35, has worked for many years as a salesman in a small used car dealership. He earns $70,000 a year. He has no group insurance at work and no individual insurance. Single and without children, his priority is to save enough money to retire at age 60. He makes regular contributions to his RRSPs, in which he has accumulated $400,000. He owns a condo valued at $250,000 on which he has an uninsured mortgage of $150,000. What financial risk is Alex most exposed to?

Dominic suffers a heart attack on October 1 and dies a little over a month later, on November 7. At the time of his death, he owned a $150,000 critical illness (CI) insurance policy, purchased 10 years earlier. Dominic never failed to pay the $100 monthly premium. When he died, the insurer had not yet issued the benefit payment.

How will the CI benefit be treated?

Vincent, aged 55, plans to retire 10 years from now after a 40-year career with the federal government. He will then receive a federal pension and will benefit from a retiree health plan. His wife Catherine is 15 years younger than him. Vincent also has an RRSP that he intends on using in part to fund his travel plans in retirement, and in part to leave a lump sum to Catherine for her living expenses after he dies. Vincent has planned his budget carefully and feels confident that he has thought of everything. What may Vincent’s insurance agent suggest he consider to safeguard his retirement?

Harper owns a disability insurance policy that will pay her a monthly benefit if she becomes unable to work. At the time she applied for the policy, Harper was a new graduate with an annual income of $60,000, and she qualified for a monthly benefit of $3,000. Instead of taking the maximum benefit, she focused on paying off her student loans and keeping her insurance premiums low. She elected to purchase a monthly benefit of $2,500 and add the future purchase option (FPO) rider for up to $500 a month of additional coverage. Now she is further along in her career, Harper earns $100,000 a year, and she meets with her insurance agent Trish to increase her coverage. Harper would like her new monthly benefit to be $5,000.

Which of the following statements about Harper’s coverage is TRUE?

Kevin owns a construction business and wants to take out accident and sickness insurance to protect his income in the event of disability. On his application form, he indicated that he had competed in motocross races over the past five years. What requirements does Kevin need to comply with before the insurer can issue the policy?

Vladimir is a new insurance agent with Family-Assure Inc. He and his supervisor Petros are reviewing the information collected during Vladimir's first meeting with Vanessa, a restaurant owner looking to add to her existing disability insurance (DI) coverage. Petros notices an overlap among sources, although the existing coverage appears adequate. Petros reminds Vladimir to explain to Vanessa how she would be impacted if she were to claim disability benefits.

What should Vladimir tell Vanessa?

Diane is an insurance agent working for Gamma Insurance Inc. who is responsible for coaching a newly licensed agent, Wick. Wick has questions about his role, and he would like to know how he should service his clients.

What should Diane tell Wick about what is expected of him?

Pat, a 30-year-old youth worker, meets with his life insurance agent to discuss disability insurancecoverage. After a thorough analysis of Pat’s needs, the agent recommends a policy with a $1,500 a month benefit (50% of Pat’s current salary) payable to age 65 after a 31-day waiting period. Pat has put enough money away to cover 6 months’ worth of expenses, if necessary, but he would prefer not to dip into his savings. He applies for the policy, with the expectation that the premium will be $75 a month. He already thinks this is pricey and would not want to pay any more than that. Some time later, underwriting informs the agent that the policy has been approved, but with a 125% premium rating due to Pat being overweight. Which one of the following options would make the most sense to reduce the premium to a level Pat would accept without compromising too much on his coverage?

Tyler, a group insurance agent, is meeting with Yolanda, the director of his new group insurance client, Compact Funds Inc., to set up the company’s plan. Compact Funds employs over 30 employees, and Tyler recommends that they implement a contributory plan. Yolanda would like to understand what this means. Which of the following statements about contributory plans is CORRECT?

Eric is an architect who owns his own firm. He employs three staff and is in his fifth year of operation. While recently meeting with his insurance agent for an annual review of his coverage, he mentioned to the agent that he had recently purchased a new printing system and has a sizeable loan on it. In the event of disability, what type of insurance coverage could the agent suggest to ensure the loan payments are made?

Dorothy, age 36, is an architect. She runs her own office with the help of two assistants. She owns her own condo, has an active social life, and travels regularly for pleasure. She has a net annual income of approximately $125,000, once all the business, rent, salary, and car expenses have been paid. Dorothy is well aware of the significant financial problems that she would face for any absences from the office due to illness or disability. What are Dorothy’s main protection needs in this respect?

Denise, age 45, is a member of her employer’s group insurance plan, which provides disability protection for 60% of her annual salary of $60,000. Louis, her 42-year-old spouse, is self-employed, has an annual income of $45,000, and no disability protection. As parents of three teenagers, Denise and Louis need $6,000 a month to meet their financial obligations with respect to such expenses as housing, food, car, clothing, and entertainment. Which of the following best characterizes Denise and Louis’ current protection?

Rowan works for a construction company that employs 40 employees. The company is newly established, and the owners have yet to implement a group insurance policy. Rowan falls off the side of a building and breaks his collar bone. The doctor informs him that he will be unable to work for five months.

Who will pay him disability benefits while he is recuperating?

Juniper, 69, suffered a stroke a few weeks ago which left her partially paralyzed and has severely reduced her mobility. Since the stroke, she is unable to leave her home. She benefits from regular visits from nurses, massage therapists, and housekeepers. Juniper wants to claim the services on her long-term care (LTC) insurance policy and would like to know how the claim will be processed and paid.

Which of the following answers is CORRECT?

On June 5, Karl completed an application for critical illness coverage and paid an annual premiumof $1,250. On June 25, the underwriter approved the policy under standard conditions and sent it to the agent, who received it on July 7. The agent contacted the client on August 8 and the date for delivery was set at August 10. On August 12, Karl learns that he will lose his job at the end of the month. As such, he decides to cancel the policy, returning it to the insurer on August 15. What is the rule governing Karl’s right to have his premium refunded?

Jordan, a group insurance agent, meets with Nancy, a commercial berry grower in Saskatoon, to renew her company's group insurance plan. When the plan was established four years ago, Nancy had 20 employees. She now has over 50 employees, many of whom are unhappy with the plan. Jordan wants to rectify this situation to everyone’s satisfaction but is not sure how to begin.

Which of the following options indicates the first step that Jordan should take?